Chart Book (6th edition): Employment and Income – Retirement Plans in Construction and Other Industries

Construction workers are less likely than workers in most other industries to be eligible for, or participate in, a retirement plan through their employment. In 2015, about a third (33.7%) of wage-and-salary construction employees were eligible to participate in an employment-based retirement plan, and only 27.4% actually participated (chart 27a).1 These rates have been continuously declining; eligibility and participation were at 38% and 33% in 2010, and 46% and 39% in 2000.2

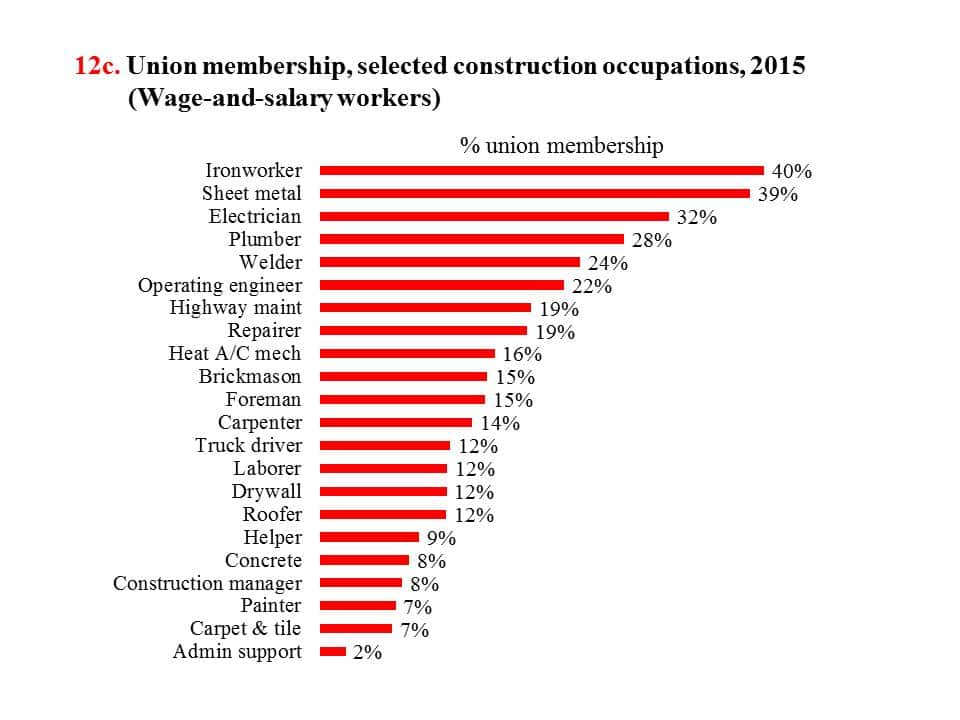

Older workers are more likely to have retirement plans. In 2015, 36% of construction workers age 50 years and over participated in retirement plans, compared to 22% among workers under age 50. Similar patterns were found in other industries; about 45.0% of workers age 50 years and over participated in retirement plans; while only 32.6% of workers under age 50 did so. Participation in a retirement plan is generally lower among construction workers employed in production occupations than those in white-collar occupations (25.3% versus 34.1%).1 However, construction production workers who belonged to a union were eligible for and participated in retirement plans at a much higher rate than did non-union workers (55.1% versus 25.9% for eligibility, and 47.4% versus 20.9% for participation; chart 27b). Construction occupations with higher unionization rates also had higher rates of participation in retirement plans. Participation was highest among sheet metal workers (55.4%), highway maintenance workers (49.9%), ironworkers (47.9%), and welders (47.9%; chart 27c; see chart 12c for union membership by occupation).

{kind=link}

Retirement plan participation varies by company size. In 2015, only 10% of construction workers who worked for companies with fewer than 10 employees participated in retirement plans.1 In contrast, 49% of construction workers employed by companies with 500 or more employees participated in retirement plans.1 Unionized construction trades typically use a multiemployer plan (see Glossary) model to fund retirement. Contractors that have signed a collective bargaining agreement with a building trades union pay into a fund that is managed jointly by trustees from the union and the employers, using investment advisors to guide their decisions. Multiemployer retirement plans may take the form of a defined benefit pension plan (see Glossary), which guarantees a level of income at retirement. There are about 1,400 multiemployer defined benefit pension plans, covering about 10 million participants. Many of these participants are employed by small companies in the building and construction industries.3 Another type of retirement plan is a defined contribution retirement plan (see Glossary), such as a 401(k) plan. Multiemployer retirement plans are common among unionized workers in other industries where workers are more likely to change employers frequently, such as trucking, grocery stores, and garment manufacturing businesses.3

Retirement information is collected by the U.S. Department of Labor (DOL) through Form 5500.4 According to the DOL, 4.42 out of 7.14 million, or 62% of retirement plan participants in construction were enrolled in multiemployer retirement plans (including both defined benefit pension plans and defined contribution retirement plans) in 2014 (chart 27d). The data also show that 96% of the 51,260 retirement plans in construction were defined contribution plans, and 61.9% of construction workers that had retirement plans participated in that type of plan.4 Overall, 93.5% of the retirement plans in the U.S. were defined contribution plans, and 71.5% of participants had such plans.

The retirement plan system in the U.S. has shifted away from defined benefit plans in favor of defined contribution plans (primarily the 401(k) plan) over the past several decades.5,6 This means that employers have shifted their responsibility for workers’ retirement onto the workers. Information on retirement plans is also available from other data sources (see page 23). Estimates are generally consistent across sources; construction employers are less likely to provide retirement benefits to their employees than all industries on average.

(Click on the image to enlarge or download PowerPoint or PDF versions below.)

Glossary:

Defined benefit pension plans – A retirement plan that uses a specific predetermined formula to calculate the amount of an employee’s future benefit. Benefits are based on a percentage of average earnings during a specified number of years at the end of a worker’s career, rather than based on investment returns. However, a new type of defined benefit plan, a cash balance plan, is becoming more prevalent. In the private sector, defined benefit plans are typically funded exclusively by employer contributions. In the public sector, defined benefit plans often require employee contributions.

Defined contribution retirement plans – A retirement plan in which the amount of the employer’s annual contribution is specified. Benefits are based on employer and employee contributions, plus or minus investment gains or losses on the money in the account. The most common type is a savings and thrift plan. Under this type of plan, the employee contributes a predetermined portion of his or her earnings (usually pre-tax) to an individual account, all or part of which is matched by the employer. Examples of defined contribution plans include 401(k) plans, 403(b) plans, employee stock ownership plans, and profit-sharing plans.

Multiemployer plan – A multiemployer plan is a collectively bargained plan maintained by more than one employer, usually within the same or related industries, and a labor union. These plans are often referred to as “Taft-Hartley plans” (ERISA Secs. 3(37) and 4001(a)(3)). The Multiemployer Pension Reform Act of 2014 (MPRA) was enacted on December 16, 2014. In the new law, Congress established new options for trustees of multiemployer plans that will potentially run out of money. Additional information on multiemployer plans is available at http://www.pbgc.gov/prac/multiemployer/introduction-to-multiemployer-plans.html.

1. Unless otherwise noted, numbers used in the text are from the U.S. Bureau of Labor Statistics, 2016 Current Population Survey (CPS), Annual Social and Economic Supplement (or March Supplement). Calculations by the CPWR Data Center. The survey asks respondents if they are offered a retirement plan at their workplace, if they are eligible to join, and if they participate. Since information on the type of plan is not available from the CPS, estimates based on the CPS data may include plans with employer contributions and plans funded solely by an employee’s personal contributions (such as a 401(k)). The CPS does not ask reasons for non-participation in such plans. In general, non-participation may result if: 1) an employee is not eligible because the job or position is not covered or the employee has not been on the job long enough, or 2) an employee chooses not to participate because the plan requires employee contributions.

2. CPWR – The Center for Construction Research and Training. 2013. The Construction Chart Book, The U.S. Construction Industry and Its Workers, fifth edition. CPWR: Silver Spring, MD. /publications/construction-chart-book (Accessed January 2017).

3. Pension Benefit Guaranty Corporation. Introduction to multiemployer plans. http://www.pbgc.gov/prac/multiemployer/introduction-to-multiemployer-plans.html (Accessed January 2017).

4. U.S. Department of Labor, Employee Benefits Security Administration. 2016. Private Pension Plan Bulletin, Abstract of 2014 Form 5500, Annual Reports. The DOL requires that retirement plans having 100 or more participants must submit Form 5500 annually.

5. Works R. 2016. Trends in employer costs for defined benefit plans. Beyond the Numbers: Pay & Benefits, 5(2). https://www.bls.gov/opub/btn/volume-5/trends-in-employer-costs-for-defined-benefit-plans.htm (Accessed January 2017).

6. Dong XS, Wang X, Ringen K, Sokas R. 2017. Baby boomers in the United States: Factors associated with working longer and delaying retirement. American Journal of Industrial Medicine (in press).

Note:

Charts 27a-27c – Retirement plan coverage includes eligibility for an employer or union and if the employee was included during the previous calendar year.

Chart 27b – The percentages for non-union workers were adjusted by the CPS annual data.

Chart 27d – Participants include active, retired, and separated vested participants not yet in pay status. Beneficiaries of the participants are excluded. The number of participants includes double counting of workers who are in more than one plan. Plans are divided into defined benefits and defined contributions.

Source:

Charts 27a-27c – U.S. Bureau of Labor Statistics. 2016 Current Population Survey, Annual Social and Economic Supplement (or March Supplement). Calculations by the CPWR Data Center.

Chart 27d – U.S. Department of Labor, Employee Benefits Security Administration. 2016. Private Pension Plan Bulletin, Abstract of 2014 Form 5500, Annual Reports.